INVESTOR PRESENTATION DATED JANUARY 19, 2026

Published on January 20, 2026

Exhibit 99.2

Investor Presentation January 2026 LATAM

Cautionary Statement Regarding Forward - Looking Statements Matters discussed in this presentation may constitute forward - looking statements . Forward - looking statements include statements concerning plans, objectives, goals, strategies, future events or performance, and underlying assumptions and other statements, which are other than statements of historical facts . The words “believe,” “anticipate,” “intends,” “estimate,” “potential,” “may,” “should,” “expect” “pending” and similar expressions identify forward - looking statements . Forward - looking statements included in this presentation relate to our expectations and projections regarding our planned acquisition of Tupperware LatAm, including accretion, synergies, integration and the financial and operational results of the combined business . The forward - looking statements in this presentation are based upon various assumptions . Although we believe that these assumptions were reasonable when made, because these assumptions are inherently subject to significant uncertainties and contingencies which are difficult or impossible to predict and are beyond our control, we cannot assure you that we will achieve or accomplish these expectations . Our actual results and financial condition may differ materially from those indicated in the forward - looking statements . Therefore, you should not rely on any of these forward - looking statements . Non - IFRS Measures This presentation contains information about the following non - IFRS financial measures : consolidated earnings before interest expense, income taxes, depreciation and amortization (“EBITDA”) . We define “EBITDA” as profit for the year adding back the depreciation of property, plant and equipment and right of use assets, amortization of intangible assets, financing cost, net and total income taxes . Adjusted EBITDA also excludes the effects of gains or losses on sale of fixed assets and adds back other non - recurring expenses . EBITDA and Adjusted EBITDA are not measures required by or presented in accordance with IFRS . The use of EBITDA and Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation from, or as a substitute for analysis of, our results of operations or financial condition as reported under IFRS . We believe that these non - IFRS financial measures are useful to investors because (i) we use these measures to analyze financial results internally and believe they represent a measure of operating profitability and (ii) these measures provide more tools for analysis as they make our results comparable to industry peers that also prepare these measures . Reconciliation from EBITDA to net income, the closest comparable IFRS measure, is included in this presentation . To the extent any such reconciliation is not included, please refer to prior presentations, which can be found on our website at https : //befra . com/investor - resources/presentations . Additionally, the presentation of the combined financial information of BeFra, Tupperware Mexico and Tupperware Brazil is not in accordance with IFRS . Combined financial information consists of the mathematical addition of selected financial data of BeFra, Tupperware Mexico and Tupperware Brazil . No other adjustments are made to the combined presentation . However, we believe that for purposes of discussion and analysis, the combined financial information is useful for management and investors to assess our ongoing financial and operational performance and trends . Accordingly, in addition to presenting our results of operations as reported in our unaudited condensed consolidated financial statements in accordance with IFRS, certain tables and discussion included within this presentation also present the combined financial information . 2

1. Acquisition Summary 2. Overview of Tupperware LatAm 3. Strategic Rationale 4. Closing Remarks 3

1 – License in Argentina will be effective starting in September 2026 BeFra to acquire Tupperware’s operations in LatAm V A a c l q u u e i s C i t r i e o a n t i S o u n m f o m r a S r h y a r e h ol d e r s 1 Acquisition of operations and manufacturing plants in Mexico and Brazil which are the region’s core markets, with scale and strong profitability BeFra to have a perpetual, royalty - free, and exclusive license for the Tupperware brand in LatAm 1 Beauty Home Organization Food Containers LATAM 4

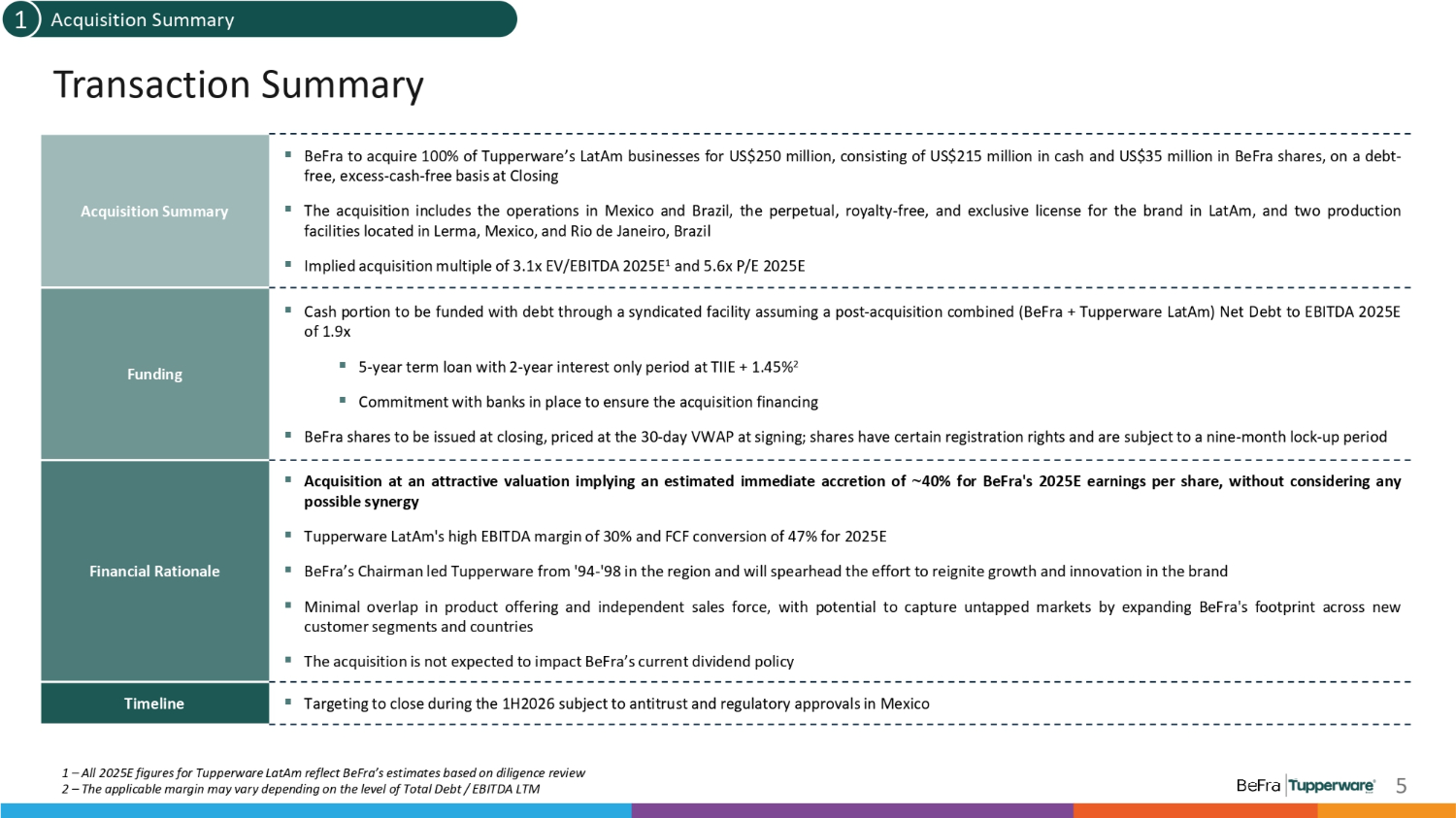

▪ BeFra to acquire 100% of Tupperware’s LatAm businesses for US$250 million, consisting of US$215 million in cash and US$35 million in BeFra shares, on a debt - free, excess - cash - free basis at Closing ▪ The acquisition includes the operations in Mexico and Brazil, the perpetual, royalty - free, and exclusive license for the brand in LatAm, and two production facilities located in Lerma, Mexico, and Rio de Janeiro, Brazil ▪ Implied acquisition multiple of 3.1x EV/EBITDA 2025E 1 and 5.6x P/E 2025E Acquisition Summary ▪ Cash portion to be funded with debt through a syndicated facility assuming a post - acquisition combined (BeFra + Tupperware LatAm) Net Debt to EBITDA 2025E of 1.9x ▪ 5 - year term loan with 2 - year interest only period at TIIE + 1.45% 2 ▪ Commitment with banks in place to ensure the acquisition financing ▪ BeFra shares to be issued at closing, priced at the 30 - day VWAP at signing; shares have certain registration rights and are subject to a nine - month lock - up period Funding ▪ Acquisition at an attractive valuation implying an estimated immediate accretion of ~ 40% for BeFra's 2025E earnings per share, without considering any possible synergy ▪ Tupperware LatAm's high EBITDA margin of 30% and FCF conversion of 47% for 2025E ▪ BeFra’s Chairman led Tupperware from '94 - '98 in the region and will spearhead the effort to reignite growth and innovation in the brand ▪ Minimal overlap in product offering and independent sales force, with potential to capture untapped markets by expanding BeFra's footprint across new customer segments and countries ▪ The acquisition is not expected to impact BeFra’s current dividend policy Financial Rationale ▪ Targeting to close during the 1H2026 subject to antitrust and regulatory approvals in Mexico Timeline Transaction Summary Acquisition Summary 1 5 1 – All 2025E figures for Tupperware LatAm reflect BeFra’s estimates based on diligence review 2 – The applicable margin may vary depending on the level of Total Debt / EBITDA LTM

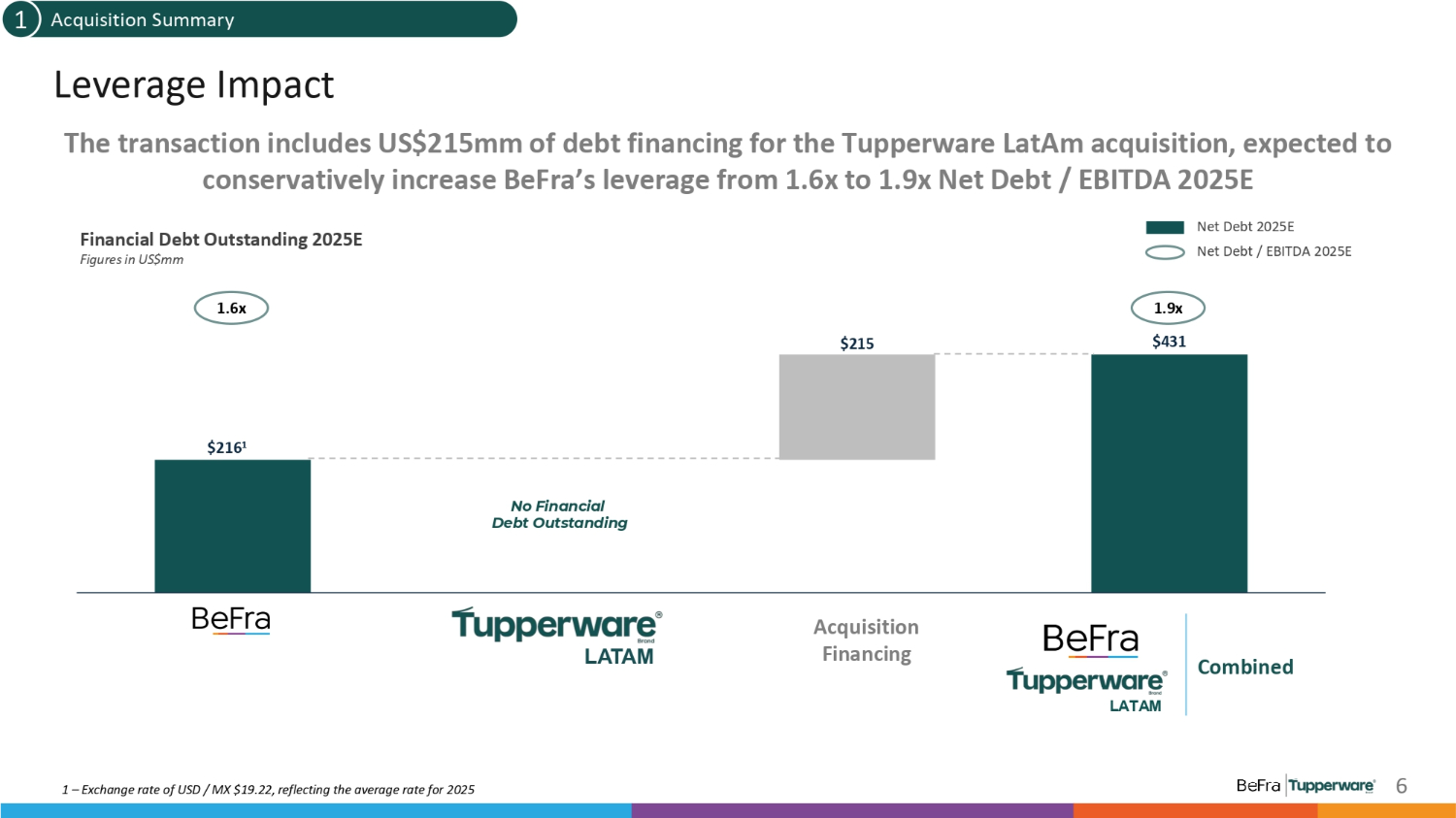

LATAM Leverage Impact $216 1 $431 $215 The transaction includes US$215mm of debt financing for the Tupperware LatAm acquisition, expected to conservatively increase BeFra’s leverage from 1.6x to 1.9x Net Debt / EBITDA 2025E Financial Debt Outstanding 2025E Figures in US$mm No Financial Debt Outstanding Acquisition Financing Combined 1.6x 1.9x Net Debt 2025E Net Debt / EBITDA 2025E 1 – Exchange rate of USD / MX $19.22, reflecting the average rate for 2025 Acquisition Summary 1 LATAM 6

1. Acquisition Summary 2. Overview of Tupperware LatAm 3. Strategic Rationale 4. Closing Remarks 7

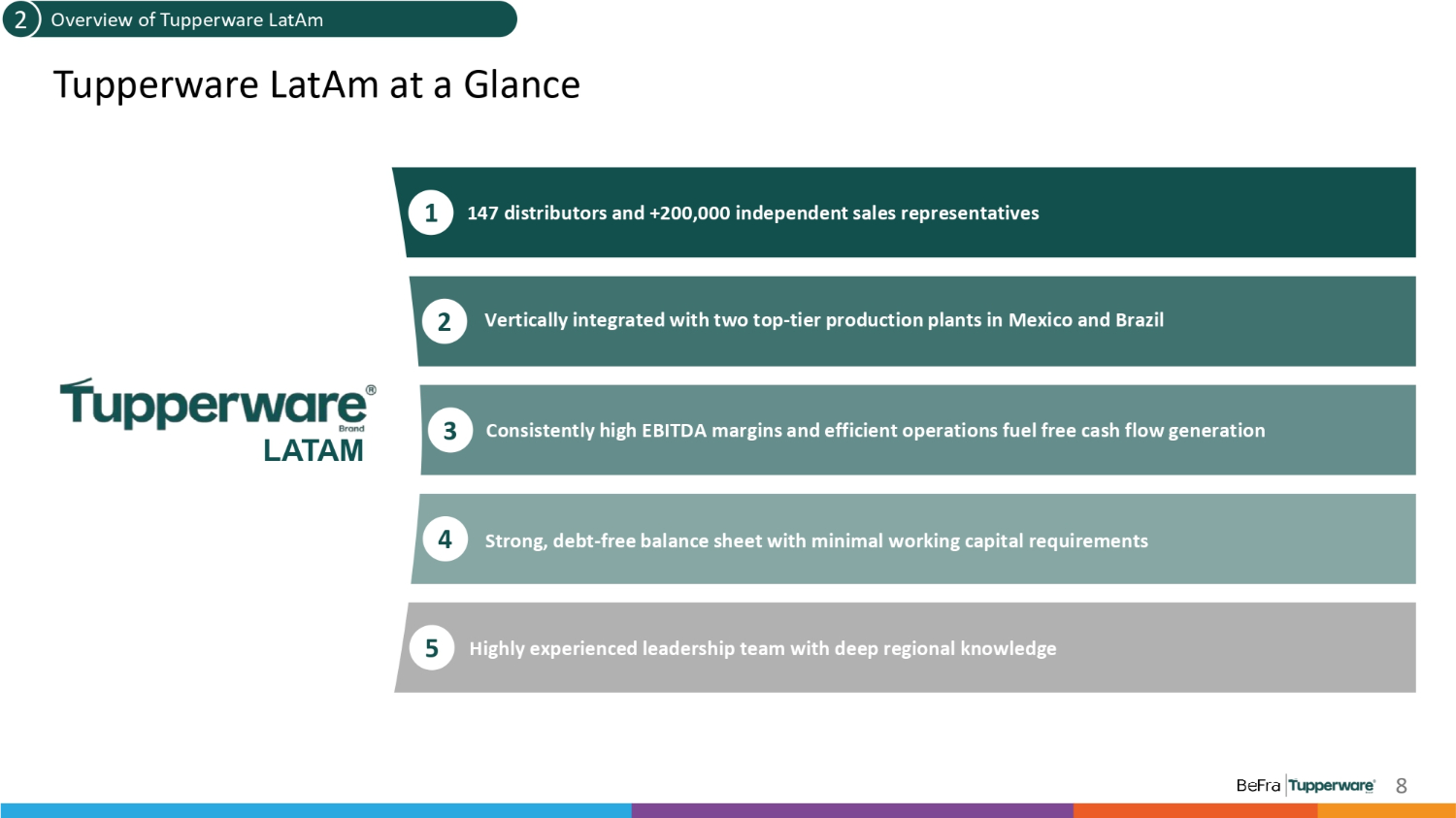

Tupperware LatAm at a Glance V O a vl e u r e v i C e r w e a o t f i o T n u p f o p r e S r w h a a r r e e h L o a l d t A e m r s 2 1 147 distributors and +200,000 independent sales representatives Highly experienced leadership team with deep regional knowledge 1 4 5 2 3 Consistently high EBITDA margins and efficient operations fuel free cash flow generation Vertically integrated with two top - tier production plants in Mexico and Brazil Strong, debt - free balance sheet with minimal working capital requirements LATAM 8

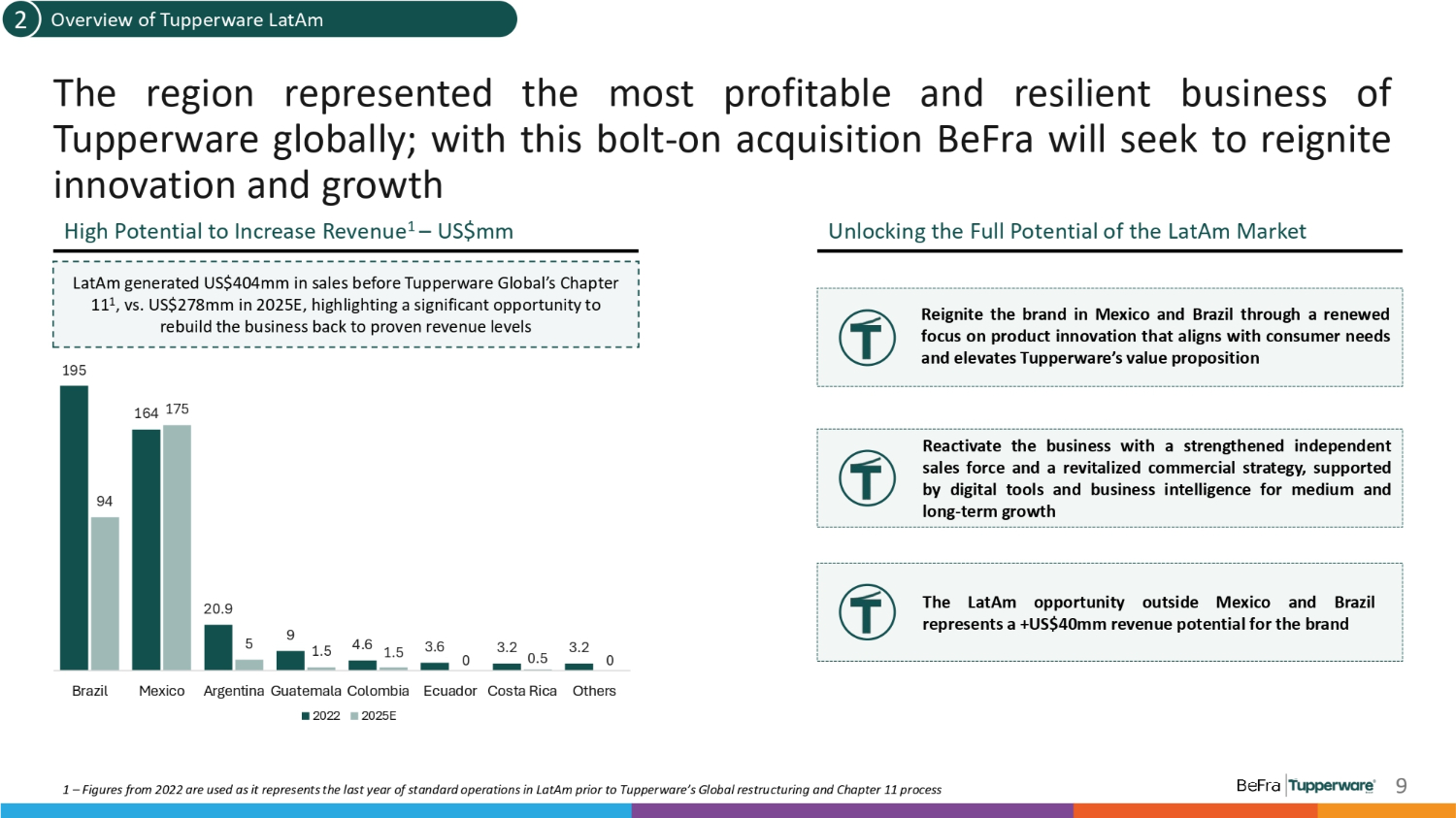

The region represented the most profitable and resilient business of Tupperware globally ; with this bolt - on acquisition BeFra will seek to reignite innovation and growth High Potential to Increase Revenue 1 – US$mm Unlocking the Full Potential of the LatAm Market 1 – Figures from 2022 are used as it represents the last year of standard operations in LatAm prior to Tupperware’s Global restructuring and Chapter 11 process LatAm generated US$404mm in sales before Tupperware Global’s Chapter 11 1 , vs. US$278mm in 2025E, highlighting a significant opportunity to rebuild the business back to proven revenue levels Reignite the brand in Mexico and Brazil through a renewed focus on product innovation that aligns with consumer needs and elevates Tupperware’s value proposition Reactivate the business with a strengthened independent sales force and a revitalized commercial strategy, supported by digital tools and business intelligence for medium and long - term growth The LatAm opportunity outside Mexico and Brazil represents a +US$40mm revenue potential for the brand 195 20.9 9 4.6 94 164 175 5 1.5 1.5 0 3.6 3.2 0.5 3.2 0 Brazil Mexico Others Argentina Guatemala Colombia Ecuador Costa Rica 2022 2025E Overview of Tupperware LatAm 2 9

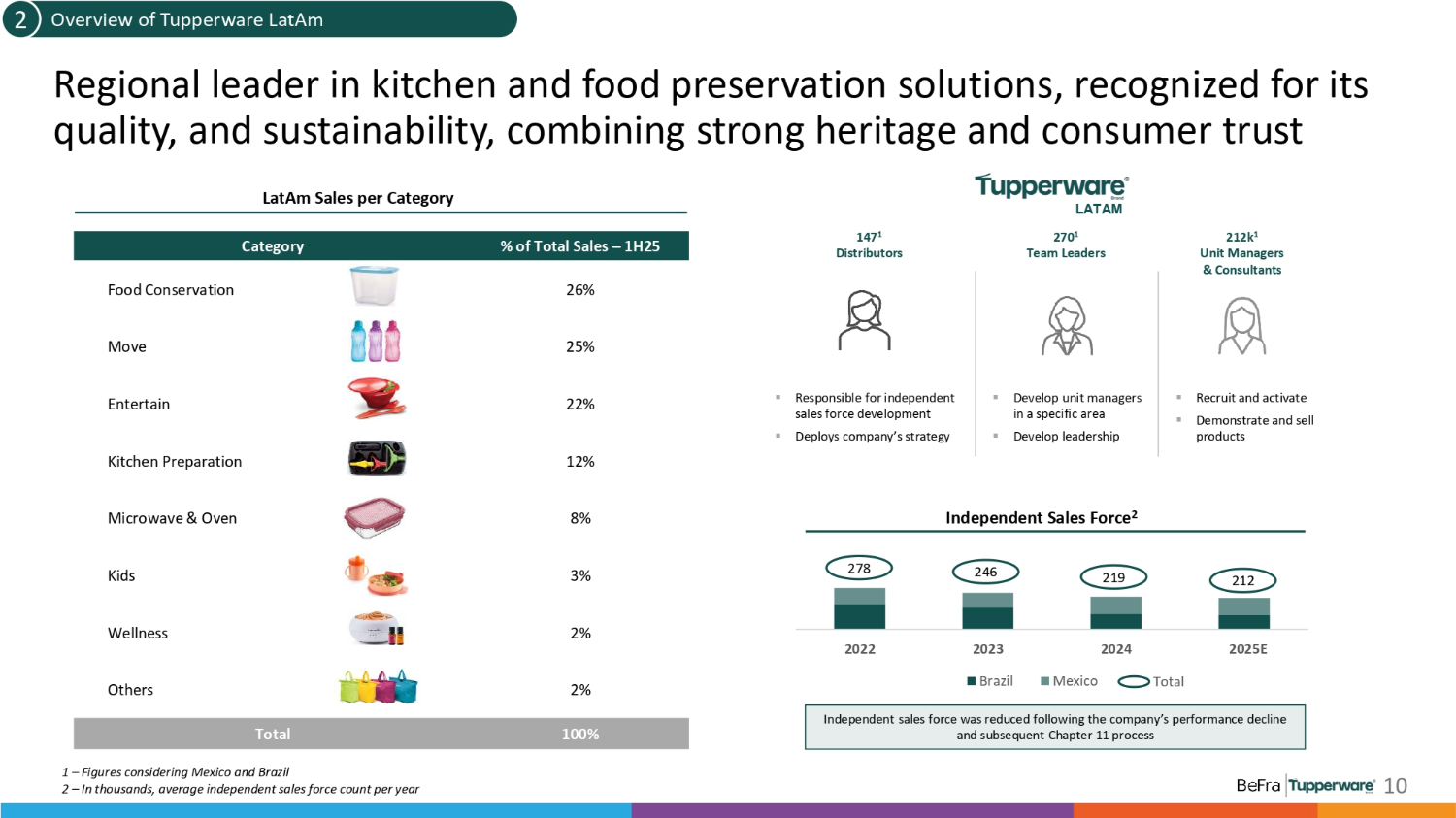

Regional leader in kitchen and food preservation solutions, recognized for its quality, and sustainability, combining strong heritage and consumer trust 147 1 Distributors 270 1 Team Leaders 212k 1 Unit Managers & Consultants Independent Sales Force 2 278 1 – Figures considering Mexico and Brazil 2 – In thousands, average independent sales force count per year Independent sales force was reduced following the company’s performance decline and subsequent Chapter 11 process ▪ Responsible for independent sales force development ▪ Deploys company’s strategy ▪ Develop unit managers in a specific area ▪ Develop leadership ▪ Recruit and activate ▪ Demonstrate and sell products % of Total Sales – 1H25 Category 26% Food Conservation 25% Move 22% Entertain Kitchen Preparation 12% Microwave & Oven 8% Kids 3% Wellness 2% Others 2% Total 100% LatAm Sales per Category Overview of Tupperware LatAm 2 LATAM 10 2022 2025E 246 219 212 2023 2024 Brazil Mexico Total

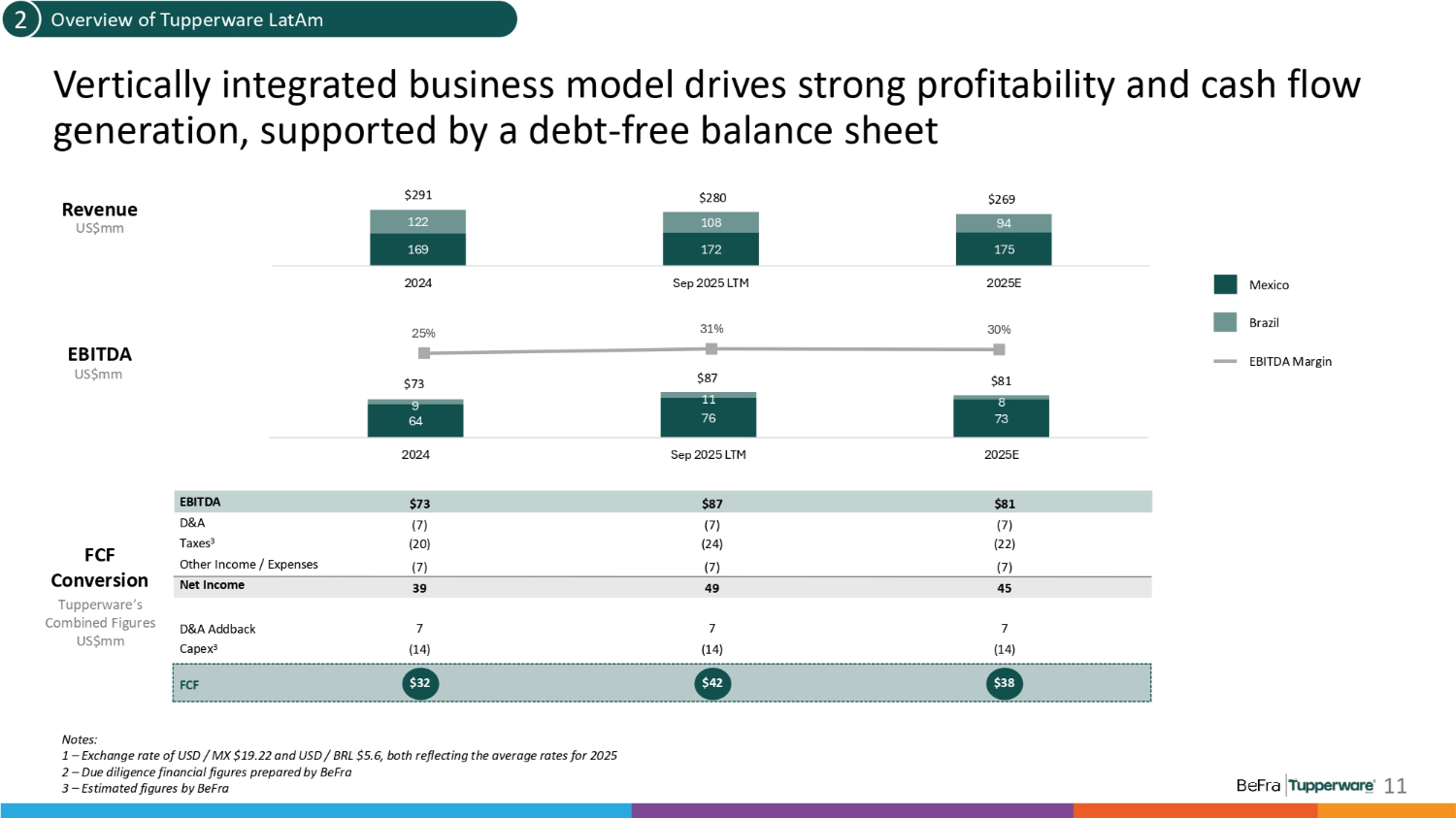

$269 $280 $291 94 108 122 175 172 169 Mexico 2025E Sep 2025 LTM 2024 Brazil EBITDA Margin 30% 31% 25% $81 $87 $73 8 73 11 76 9 64 2025E Sep 2025 LTM 2024 $81 $87 EBITDA $73 (7) (7) D&A (7) (22) (24) Taxes 3 (20) (7) (7) Other Income / Expenses (7) 45 49 Net Income 39 7 7 D&A Addback 7 (14) (14) Capex 3 (14) Vertically integrated business model drives strong profitability and cash flow generation, supported by a debt - free balance sheet Revenue US$mm EBITDA US$mm Notes: 1 – Exchange rate of USD / MX $19.22 and USD / BRL $5.6, both reflecting the average rates for 2025 2 – Due diligence financial figures prepared by BeFra 3 – Estimated figures by BeFra FCF Conversion Tupperware’s Combined Figures US$mm FCF $32 $42 $38 Overview of Tupperware LatAm 2 11

1. Acquisition Summary 2. Overview of Tupperware LatAm 3. Strategic Rationale 4. Closing Remarks 12

Foundational Drivers of Sustained Growth, Market Expansion, and Long - Term Value Creation S V t a r l a u t e e g C i r c e R a t a i t o i o n n f a o l r e Sha r e h ol d e r s 3 1 Growth 1 Significant untapped potential across Latin America, where a well - executed operational turnaround and disciplined commercial strategy can meaningfully expand Tupperware’s revenue, market share, and long - term value creation 2 Expansion 3 Capacity Experience 4 Accretion 5 13 Compelling entry into the high - growth Brazilian market, with a clear pathway to introduce the Betterware brand and unlock significant cross - market synergies, category expansion, and scale advantages Strategic manufacturing footprint in Mexico and Brazil — with strong operational readiness and significant excess capacity (35 – 40% available) — providing a compelling platform to localize production reduce supply risk and optimize costs Prior to founding BeFra, Mr. Luis Campos held senior leadership roles at Tupperware, bringing unparalleled experience to this transaction and the new business. He served as President of Tupperware Americas from 1994 to 1998 Transaction expected to be immediately accretive adding ~40% to the consolidated EPS in 2025E

A Legacy of Direct - to - Consumer Innovation: 30+ Years of Market - Shaping Expertise • Prior to founding BeFra, Mr . Luis Campos held senior leadership roles at Tupperware, bringing unparalleled experience to this transaction . He served as President of Tupperware Americas from 1994 to 1998 and as CEO of Sara Lee – House of Fuller (Tupperware’s former beauty division) from 1991 to 1993 • Together with Andrés and Santiago, the team has deep, long - standing familiarity with Tupperware’s business model , culture, and leadership team, giving them exceptional insight into the company’s operational and strategic levers • Their backgrounds enable the team to guide the integration and transition with precision while unlocking innovation and growth across Tupperware’s Latin American operations • This leadership team, backed by highly experienced Tupperware management teams in Mexico and Brazil with decades of experience , will endeavor to provide continuity, preserve the legacy of each brand, and deliver a seamless integration that positions Tupperware for long - term success in the region Luis Campos BeFra’s Chairman of the Board Andrés Campos BeFra’s CEO Santiago Campos M.D. of Betterware Mexico Strategic Rationale 3 14

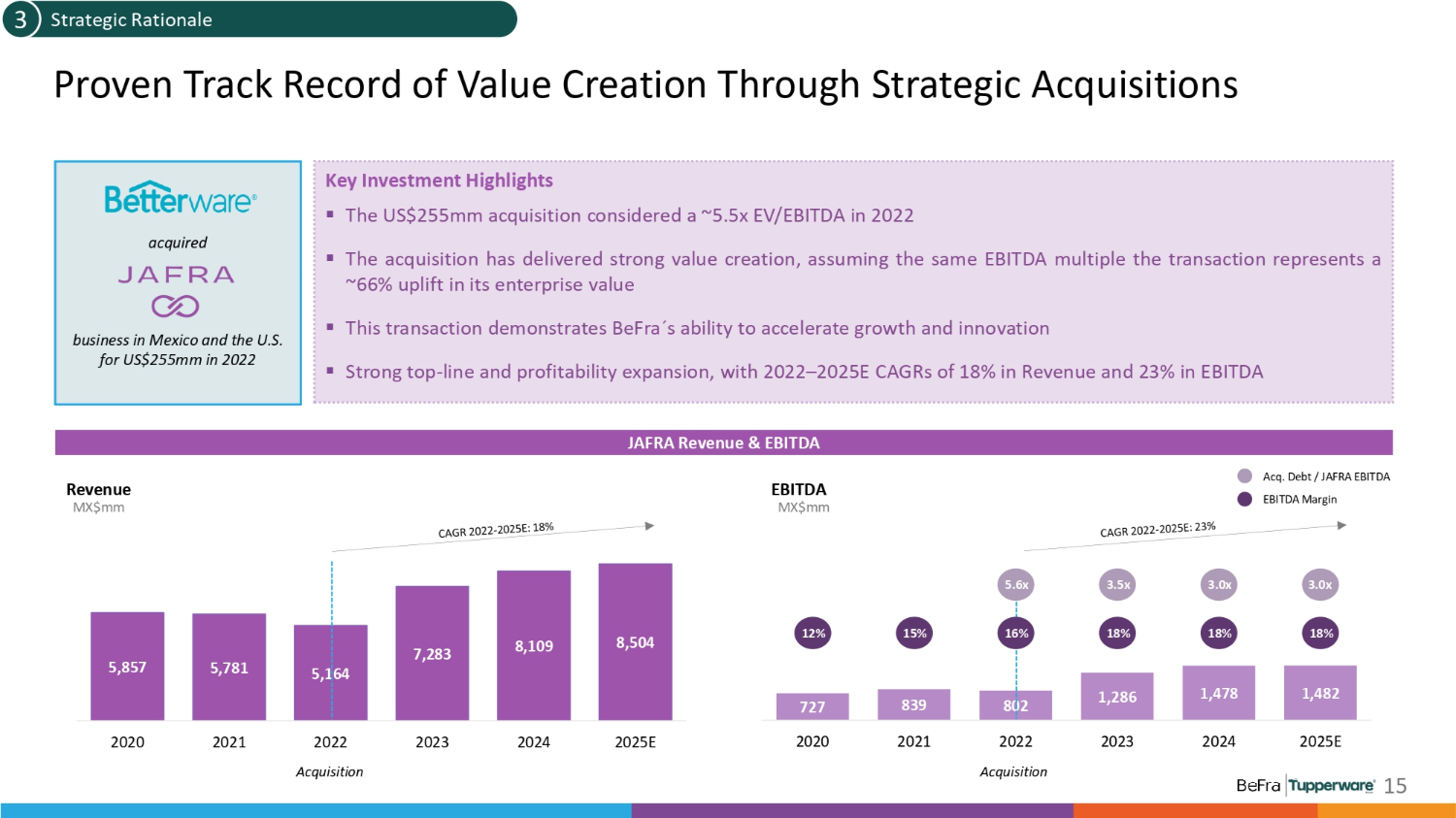

Proven Track Record of Value Creation Through Strategic Acquisitions acquired business in Mexico and the U.S. for US$255mm in 2022 JAFRA Revenue & EBITDA 5,857 5,781 5,1 64 7,283 8,109 8,504 2020 2021 2023 2024 2025E 2022 Acquisition Revenue MX$mm Key Investment Highlights ▪ The US$255mm acquisition considered a ~5.5x EV/EBITDA in 2022 ▪ The acquisition has delivered strong value creation, assuming the same EBITDA multiple the transaction represents a ~66% uplift in its enterprise value ▪ This transaction demonstrates BeFra Dz s ability to accelerate growth and innovation ▪ Strong top - line and profitability expansion, with 2022 – 2025E CAGRs of 18% in Revenue and 23% in EBITDA 727 839 802 1,286 1,478 1,482 2020 2021 2022 Acquisition 2023 2024 2025E EBITDA MX$mm 12% 15% 16% 18% 18% 18% 5.6x 3.5x 3.0x 3.0x Acq. Debt / JAFRA EBITDA EBITDA Margin Strategic Rationale 3 15

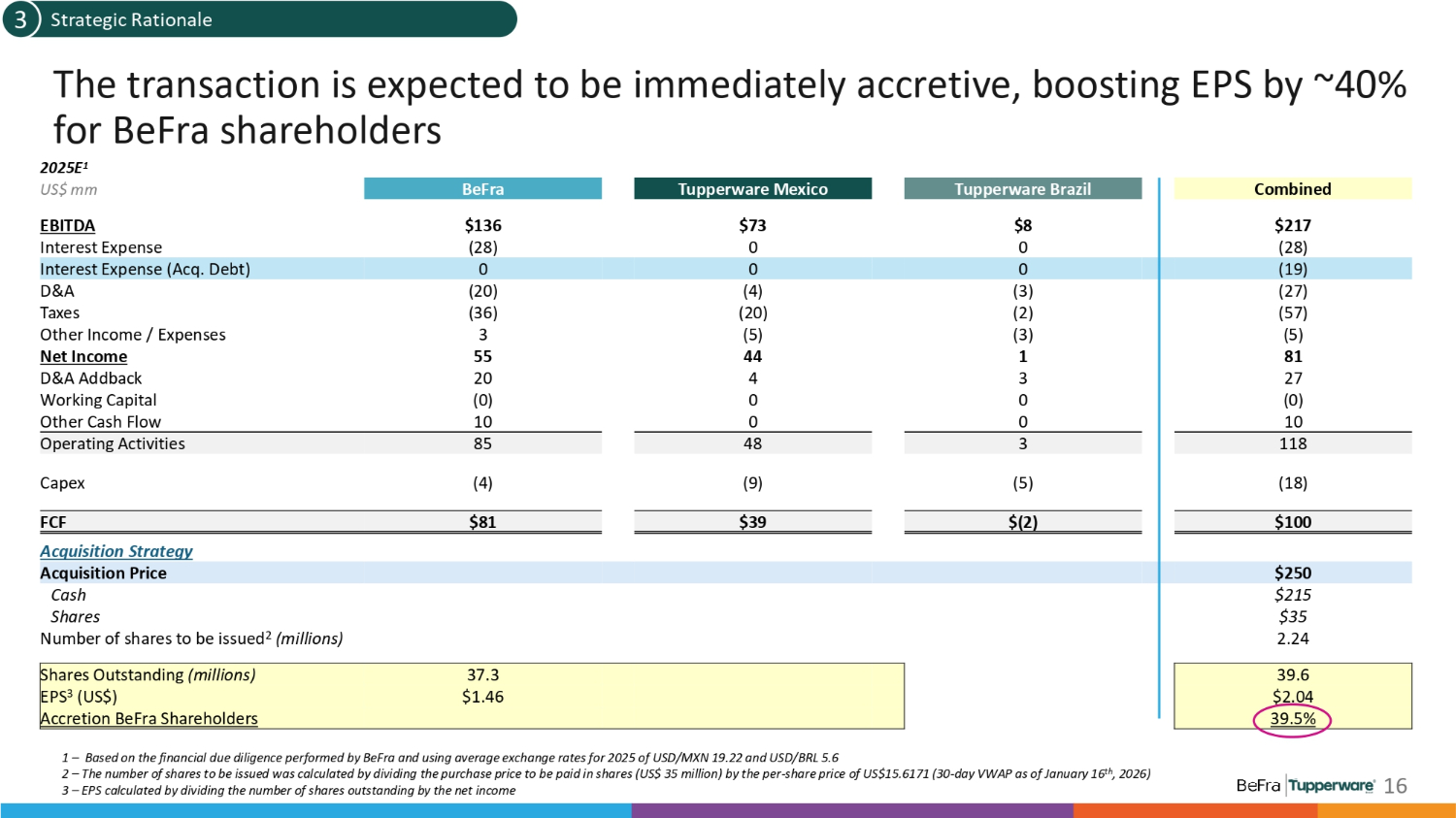

The transaction is expected to be immediately accretive, boosting EPS by ~40% for BeFra shareholders 2025E 1 Combined Tupperware Brazil Tupperware Mexico BeFra US$ mm $217 $8 $73 $136 EBITDA (28) 0 0 (28) Interest Expense (19) 0 0 0 Interest Expense (Acq. Debt) (27) (3) (4) (20) D&A (57) (2) (20) (36) Taxes (5) (3) (5) 3 Other Income / Expenses 81 1 44 55 Net Income 27 3 4 20 D&A Addback (0) 0 0 (0) Working Capital 10 0 0 10 Other Cash Flow 118 3 48 85 Operating Activities (18) (5) (9) (4) Capex $100 $(2) $39 $81 FCF Acquisition Strategy $250 Acquisition Price $215 Cash $35 Shares 2.24 Number of shares to be issued 2 (millions) 39.6 37.3 Shares Outstanding (millions) $2.04 $1.46 EPS 3 (US$) 39.5% Accretion BeFra Shareholders 1 – Based on the financial due diligence performed by BeFra and using average exchange rates for 2025 of USD/MXN 19.22 and USD/BRL 5.6 2 – The number of shares to be issued was calculated by dividing the purchase price to be paid in shares (US$ 35 million) by the per - share price of US$15.6171 (30 - day VWAP as of January 16 th , 2026) 3 – EPS calculated by dividing the number of shares outstanding by the net income 16 Strategic Rationale 3

1. Acquisition Summary 2. Overview of Tupperware LatAm 3. Strategic Rationale 4. Closing Remarks 17

L C V i a l m o l u s i t i e n e g C d r R O e e a v m t e i r o a l n a r k p f s or Shareholders 4 1 A unique opportunity to acquire a high - quality brand for the LatAm market Leverage BeFra's proven capabilities to expand the brand portfolio and geographic footprint through Tupperware Expected to create immediate shareholder value and positions the business for strong, long - term growth while maintaining BeFra's leverage below 2.0x 1 1 3 3 2 2 LATAM 18